Overview

Inheritance Tax exemptions can be achieved by means of making certain exempt transfers

You have the option to transfer some of your assets during your lifetime, which are referred to as “lifetime transfers.” However, it’s important to consider the potential implications for Inheritance Tax when making such gifts. There are two main types of lifetime transfers: potentially exempt transfers (PETs) and chargeable lifetime transfers (CLTs).

Exempt transfers

Potentially exempt transfers are lifetime gifts made directly to other individuals

PETs include gifts to Bare Trusts. A similar lifetime gift made to most other types of Trust is a chargeable lifetime transfer. These rules apply to non-exempt transfers: gifts to a spouse are exempt, so are not subject to Inheritance Tax.

Where a potentially exempt transfer fails to satisfy the conditions to remain exempt – because the person who made the gift died within seven years – its value will form part of their estate. Survival for at least seven years, on the other hand, ensures full exemption from Inheritance Tax.

Chargeable lifetime transfers are not conditionally exempt from Inheritance Tax. If it is covered by the Nil-Rate Band (NRB) and the transferor survives at least seven years, it will not attract a tax liability, but it could still impact other chargeable transfers.

Seven Year Rule

Chargeable lifetime transfers that exceed the available NRB when they are made result in a lifetime Inheritance Tax liability paid by settlor.

Failure to survive for seven years results in the value of the chargeable lifetime transfers being included in the estate. If the chargeable lifetime transfers are subject to further Inheritance Tax on death, a credit is given for any lifetime Inheritance Tax paid during life.

Following a gift to an individual or a Bare Trust (a basic Trust in which the beneficiary has the absolute right to the capital and assets within the Trust, as well as the income generated from these assets), there are two potential outcomes: survival for seven years or more, and death before then.

The former results in the potentially exempt transfer becoming fully exempt and no longer figuring in the Inheritance Tax assessment. In other cases, the amount transferred less any Inheritance Tax exemptions is ‘notionally’ returned to the estate.

Tax

Tax consequences

Anyone utilising potentially exempt transfers for tax migration purposes, therefore, should consider the consequences of failing to survive for seven years. Such an assessment will involve balancing the likelihood of surviving for seven years against the tax consequences of death within that period.

Failure to survive for the required seven-year period results in the full value of the potentially exempt transfers being notionally included within the estate; survival beyond then means nothing is included. It is taper relief which reduces the Inheritance Tax liability (not the value transferred) on the failed potentially exempt transfers after the full value has been returned to the estate.

Pareto Financial Planning are not tax specialists and further advice should be sought. Further information can be found at gov.uk

Earlier transfers

The value of the potentially exempt transfers is never tapered. The recipient of the failed potentially exempt transfers is liable for the Inheritance Tax due on the gift itself and benefits from any taper relief. The Inheritance Tax due on the potentially exempt transfers is deducted from the total Inheritance Tax bill, and the estate is liable for the balance.

Lifetime transfers are dealt with in chronological order upon death; earlier transfers are dealt with in priority to later ones, all of which are considered before the death estate. If a lifetime transfer is subject to Inheritance Tax because the NRB is not sufficient to cover it, the next step is to determine whether taper relief can reduce the tax bill for the recipient of the potentially exempt transfers.

Sliding Scale

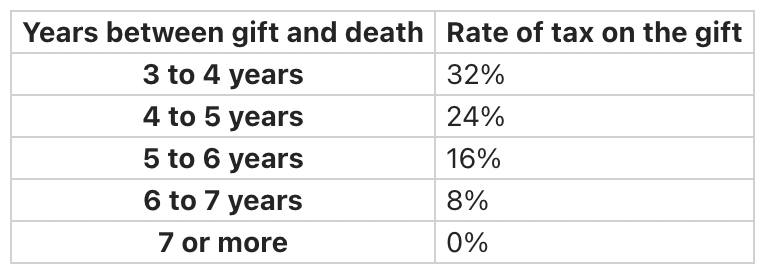

The amount of Inheritance Tax payable is not static over the seven years prior to death. Rather, it is reduced according to a sliding scale dependant on the passage of time from the giving of the gift to the individual’s death.

No relief is available if death is within three years of the lifetime transfer. For survival for between three and seven years, taper relief at the following rates is available.