Spending

Budgeting

Take Control of Your Money

Budgeting is one of the most important financial habits you can adopt.

A budget can help you control your spending, track your expenses, and save more money. Budgeting can also help you make better financial decisions, be more prepared for emergencies, and stay focused on your long-term financial goals.

Creating a budget is the first step towards taking control of your finances. A budget is a list of all the money you receive and all the things you spend money on each month.

If you’re looking for a simple way to help you manage your money and track your outgoings, you may find our free budget template useful:

Download our budget template

Once you’ve worked out how much money you’ve got coming in and how much you’re spending, you’ll spot areas where you could make savings. People often shop around for the best price when initially purchasing something like insurance and paid television subscriptions, but over time the price goes up and you don’t always continue to shop around.

Common bills that you may be able to cut or reduce include:

- Recurring subscriptions

- Phone, broadband and TV

- Utilities

- Insurances

If you are self-employed, you may have inconsistent income. Consider using your earnings from the lowest income-earning month you’ve had in the last 36 months as the baseline amount when setting up your monthly budget.

Debt

Plan to Payback Realistically

Budgeting can bring a sense of order when it comes to paying off debt. This can help debt to be more manageable to deal with. You’ll be able to identify a regular payoff goal and ways to free up money to pay off your debt.

A budget can help you concentrate on debt repayment but ensure you don’t ignore other important financial priorities. It gives you structure, a method to allocate money to emergency savings, and a clear way to reward yourself for making progress.

Find out more about borrowing

If you are feeling overwhelmed by your financial situation seek help. There are a number of charities and organisations that offer free independent advice and can help ease anxiety and help you get back on track. Look at:

National Debtline, StepChange, or Citizens Advice.

Also, the Money Saving Expert website has a debt guide which shows you where to start and how to get free one-on-one help.

Pareto does not offer debt advice or debt counselling as part of its services.

Saving

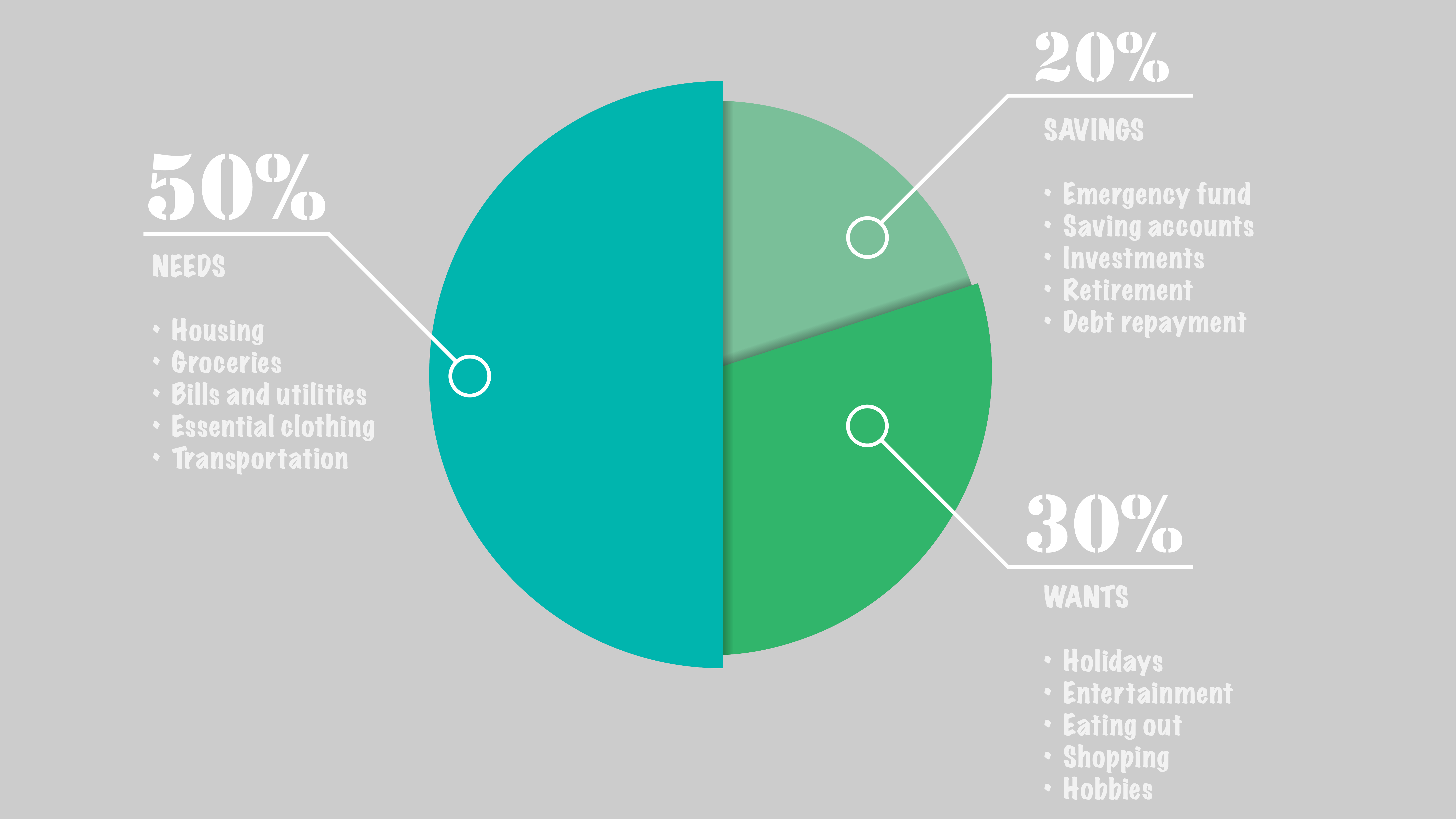

The 80/20 Rule

It’s not easy juggling a tight budget but if you have surplus money in your budget, you could consider saving or investing.

In an ideal world, 20% of your monthly income would be put towards your savings. You should review your savings account at least once a year to check you’re getting the best rate of interest. Also, consider using your annual Individual Savings Account (ISA) allowance so that you don’t pay tax unnecessarily

The 80/20 rule can be split down further still to help you with budgeting:

Whilst these rules are useful guides, everyone’s situation is different, and some people may find that their spending doesn’t fit these rules.

Find out more about saving

Tips

Good to Remember

Some quick fix tips when you are creating or reviewing your budget:

- Check recurring subscriptions – do you need/use them all?

- Review utilities, phone, broadband and insurance costs – are there any better deals available?

- Check the standing orders/direct debits on your account for any auto-renewals you no longer want

- Utilise any discount codes when shopping – some employee benefits platforms offer money off your weekly shop as well as bigger purchases

- Plan your meals for the week so you have less wastage and are less likely to end up getting takeaway!

- Some cashback sites offer to pay if you spend through them and some credit cards offer annual cashback. Whilst cashback sites can generate some users money, it is very important to understand, before you start to use them, that there can be substantial pitfalls when using such sites.

What is inflation?

Purchasing Power

Inflation is the term we use to describe rising prices. The rate of inflation is the change in prices for goods and services over time. A low and stable rate of inflation helps to create a healthy economy.

The Government sets a target for how much prices overall should go up each year in the UK. That target in 2022 is 2%. It’s the Bank of England’s job to keep inflation at that target.

A little bit of inflation is helpful. But high and unstable rates of inflation can be harmful. If prices are unpredictable, it is difficult for people to plan how much they can spend, save or invest.

Our video below helps explain inflation:

There’s no sure way to protect your money from the effects of inflation.

Cash savings accounts are generally not the best places to put your money long-term as inflation reduces buying power of money over time.

But if you’re planning to put money aside for five years or more, it might be better to invest. There are an increasing number of investment opportunities for beginners, even if you don’t have thousands to invest.

However, the value of investments and the income from them can go down as well as up and you may not get back the amount originally invested. Understanding inflation is crucial to investing because inflation can reduce the value of investment returns. Investing may not be suitable for all.

Benefits

Financial Support

Benefits and tax credits are payments from the government to certain people on low incomes, or to meet specific needs. Further information is available at gov.uk. They can help you if you:

- Are on a low income

- Are sick or disabled

- Are out of work

- Are pregnant

- Have children

- Have been bereaved

- Are a carer

The UK’s benefits system is very complicated and it can feel overwhelming for people using it for the first time. Free online resources e.g. benefits calculators can help you estimate your entitlement to benefits.

As the cost of living continues to affect households across the UK, the government has also announced a new package of payments to help most families claiming benefits.

Find out what support is available to help with the cost of living here. This includes income and disability benefits, bills and allowances, childcare, housing and travel.