Overview

Protecting family wealth with trusts

Trusts protect family wealth for future generations, reducing the inter-generational flow of Inheritance Tax and ensuring bloodline protection for your estate from outside claims.

The way in which assets held within Trusts are treated for Inheritance Tax purposes depends on whether the choice of beneficiaries is fixed or discretionary. The most popular types of Trust commonly used for Inheritance Tax planning can usually be written on an ‘absolute’ or a ‘discretionary’ basis. The taxation treatment is very different for each.

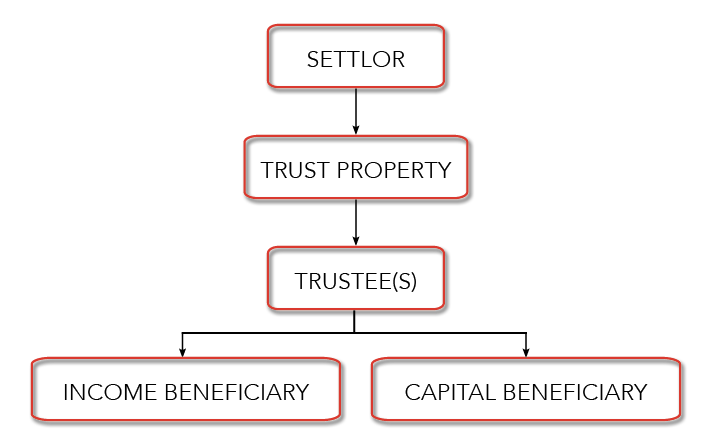

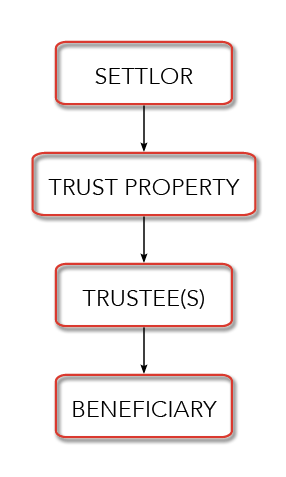

A Trust is a fiduciary arrangement that allows a third party, or trustee, to hold assets on behalf of a beneficiary or beneficiaries. Once the Trust has been created, a person can use it to ‘ring-fence’ assets.

Trust terms:

- Settlor – the person setting up the Trust.

- Trustees – the people tasked with looking after the Trust and paying out its assets.

- Beneficiaries – the people who benefit from the assets held in Trust.

Making use of Trusts

Assets can be put in an appropriate Trust, thereby no longer forming part of the estate. Many types of Trust available can be set up simply at little or no charge. They usually involve parents (settlors) investing money into a Trust.

The Trust has to be set up with trustees – a suggested minimum of two – whose role is to ensure that on the death of the settlors, the investment is paid out according to the settlors’ wishes.

In most cases, this will be to children or grandchildren. The most widely used Trust is a Discretionary Trust, which can be set up so that the settlors (parents) still have access to income or parts of the capital.

It can seem daunting to put money away in a Trust, but it can be unwound in the event of a family crisis and monies returned to the settlors via the beneficiaries.

Types

Bare Trust

Bare Trusts are also known as ‘Absolute’ or ‘Fixed Interest Trusts’, and there can be subtle differences. The settlor – the person creating the Trust – makes a gift into the Trust which is held for the benefit of a specified beneficiary.

If the Trust is for more than one beneficiary, each person’s share of the Trust fund must be specified. For lump sum investments, after allowing for any available annual exemptions, the balance of the gift is a potentially exempt transfer for Inheritance Tax purposes.

As long as the settlor survives for seven years from the date of the gift, it falls outside their estate.

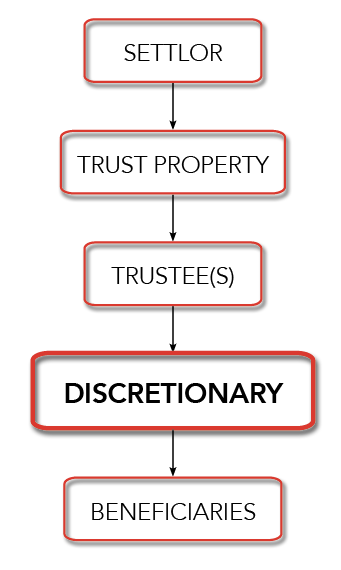

Discretionary Trust

With a Discretionary Trust, the settlor makes a gift into Trust, and the trustees hold the Trust fund for a wide class of potential beneficiaries. This is known as ‘settled’ or ‘relevant’ property. For lump sum investments, the initial gift is a chargeable lifetime transfer for Inheritance Tax purposes.

It’s possible to use any available annual exemptions. If the total non-exempt amount gifted is greater than the settlor’s available nil- rate band, there’s an immediate Inheritance Tax charge at the 20% lifetime rate – or effectively 25% if the settlor pays the tax.

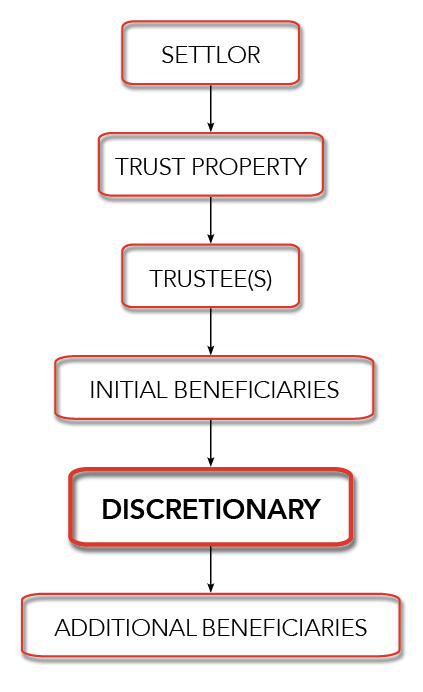

Flexible Trusts with Default Beneficiaries

Flexible Trusts are similar to a fully Discretionary Trust, except that alongside a wide class of potential beneficiaries, there must be at least one named default beneficiary.

Flexible Trusts with default beneficiaries set up in the settlor’s lifetime from 22 March 2006 onwards are treated in exactly the same way as Discretionary Trusts for Inheritance Tax purposes.

Different Inheritance Tax rules apply to older Trusts set up by 21 March 2006 that meet specified criteria and some Will Trusts. All post-21 March 2006 lifetime Trusts of this type are taxed in the same way as fully Discretionary Trusts for Inheritance Tax and Capital Gains Tax purposes.

Split Trusts

Split Trusts are often used for family protection policies with critical illness or terminal illness benefits in addition to life cover.

Split Trusts can be Bare Trusts, Discretionary Trusts, or Flexible Trusts with default beneficiaries. When using this type of Trust, the settlor/life assured carves out the right to receive any critical illness or terminal illness benefit from the outset, so there aren’t any gifts with reservation issues (i.e. a situation where a person gives away property, but still retains some right or benefit over it).

In the event of a claim, the provider normally pays any policy benefits to the trustees, who must then pay any carved-out entitlements to the life assured and use any other proceeds to benefit the Trust beneficiaries.